The Broken Model: Why Traditional Wealth Advisory No Longer Works

The Art of Selling Smart: A Strategy for Every Market

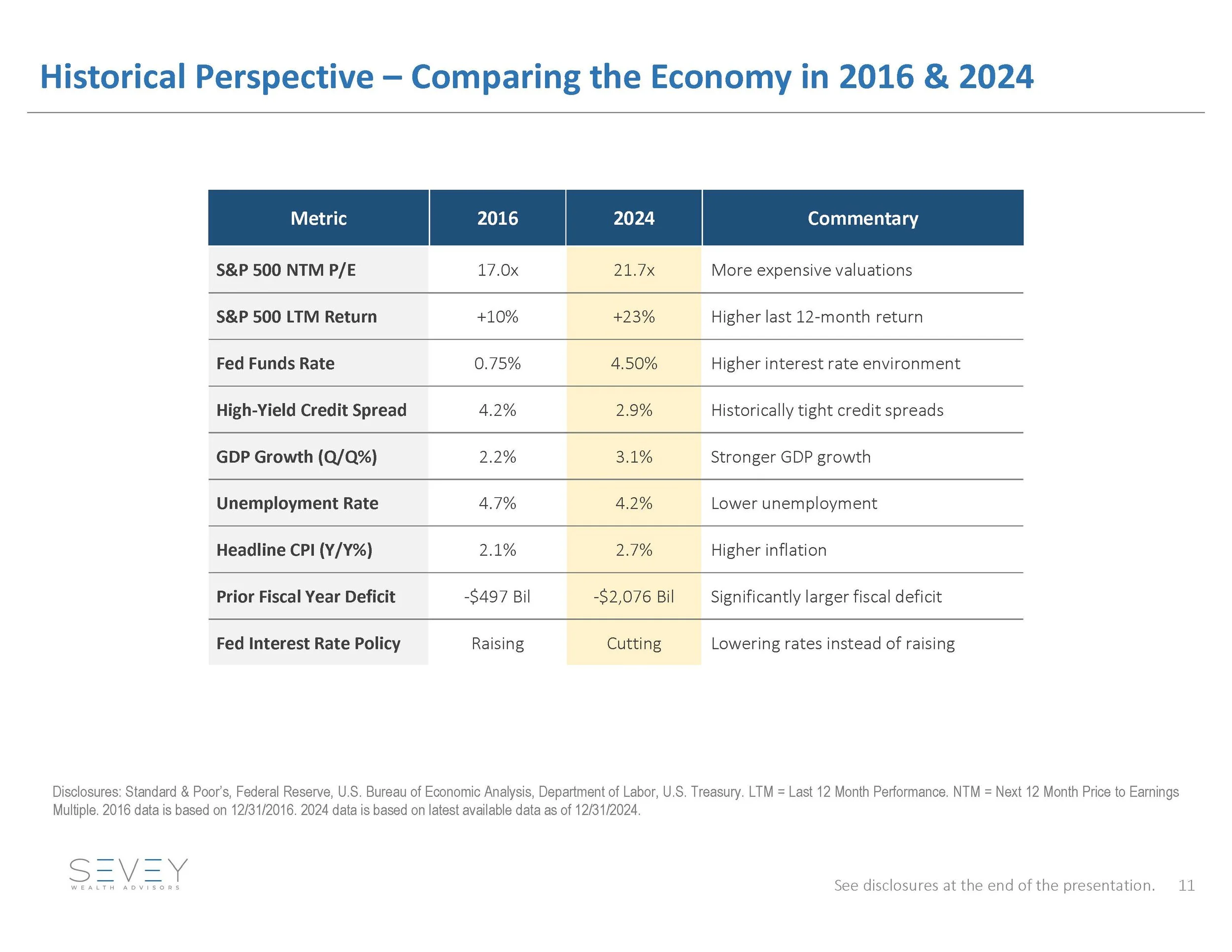

What to Expect from the New Trump Administration: A Market Perspective

Why I Prefer Retirement Buckets vs The Systematic Withdrawal Plan

Unless you have enough money to live off just the interest of your portfolio, you will need to choose between a systematic withdrawal plan and utilizing retirement buckets to provide your retirement income.

Here is why I prefer the retirement buckets strategy:

How To Plan For Down Markets…In My Opinion.

We all know investing includes ups and downs. Mostly up… but not always. It’s a natural part of investing. But lately, with the recent run in stocks and concerns rising about a pullback, I have been having more conversations about how to plan for a pullback.

To me, the best approach to volatility is to be bipolar: Fiercely protective over any money you will need in the next couple of years and aggressive with investments that you do not need to draw from for some time.

Is Your Portfolio Built Around Your Goals or Their Model?

Throughout my 24-year tenure as an advisor, my preference has leaned towards a Goal-Based investment strategy and plan as opposed to an asset allocation model portfolio, and this inclination is grounded in several reasons.

While Goal-Based investing and Model Portfolios both prove to be valid and successful investment strategies, they distinctly differ in their approaches and intended purposes.

How Does Your Financial Advisor Get Paid?

In the complex world of financial planning and investment management, one crucial question often goes unasked: How does your financial advisor get paid? The answer to this question can significantly impact the quality of advice you receive and, ultimately, your financial success. This white paper explores various fee structures for financial advisors, with a particular focus on how flat fee-based advisors provide a superior structure compared to traditional fee-only Assets Under Management (AUM) managers, especially for clients with higher net worth.

Teaching Children How to Build Credit

As parents, we strive to equip our children with the knowledge and skills they need to navigate the complexities of adulthood successfully. One crucial aspect of financial literacy that often gets overlooked is building credit.

By teaching children and teens about credit from an early age, we can empower them to make wise financial decisions and lay a solid foundation for their financial future. Let’s explore some practical tips on how to get children and teens started on the right path:

When Do Annuities Make Sense (Almost Never!)

When do annuities make sense in a portfolio? In my opinion, rarely! After over two decades of experience, I personally feel the drawbacks of annuities fail the Fiduciary Standard that clients are entitled to. Here are the 5 reasons I avoid using annuities:

Is Asset Allocation Broken?

The basis of Asset Allocation was formed in 1952. Numerous advances and complexities have been added to the investing landscape since then while the core concept has largely remained unchanged. While Modern Portfolio Theory (MPT) has been widely influential in investment management, it is not without its limitations and criticisms. Here are some of the downsides associated with MPT:

Is Robo Advice Too Simple?

Robo advisors offer several benefits, such as low fees, automated portfolio management, and simplified investment options. However, there are a few potential downsides associated with using robo advisors. Here are some considerations:

Claiming Social Security While Working

Understanding when and how to claim Social Security benefits isn’t always straightforward, especially if you plan to continue working. While you can start collecting benefits as early as age 62, continuing to work before you reach your full retirement age (FRA) may impact how much you can collect.

What is Flat Fee Wealth Management?

Flat fee wealth management is a financial advisory model that charges clients a fixed fee based on the services provided, rather than a percentage of their assets under management (AUM). This approach has gained popularity in recent years due to its simplicity, transparency, and potential cost savings for investors.

Talking to your Aging Parents about Finances

For many families, finances are rarely discussed in detail, even as children mature into adulthood. But as your parents age, especially if they live into their 80s and 90s, there's a chance that they may lose their cognitive function and be less capable of managing various tasks. This can be upsetting for some parents and they may try to fight it, or deny that it’s happening.

Should You Have a Living Trust?

A will is the foundation of your estate plan and it is essential if your financial affairs are to be settled in accordance with your wishes. If you die without a will, or “intestate” as the law refers to it, essentially the state becomes your executor and your property will be distributed according to its laws. Drawing up a will has become so easy, and it is relatively inexpensive, leaving very little reason why everyone shouldn’t have one. The question becomes whether you should have a living trust in addition to your will.

Document Retention

Is your garage overflowing with bank statements and paid bills from ten years ago? Are you unsure about what documents need to be retained and what can be tossed? Speaking of tossing, what documents can be tossed in the trash, and which should be shredded? Are you wanting to finally get control of your documents? If so, here are some suggestions for getting that paper under control today.

Preparing for Lifetime Income in Retirement

There was a time when old retirement planning models like “the 70 percent rule” were more common. This rule stated that a retiree only needed 70% of their pre-retirement income to live comfortably in retirement. More common is the 4% rule that states you can comfortably retire if your spending is capped at 4% of your liquid assets. These “rules” may have worked for some retirees several decades ago but can be dangerously flawed in today’s new normal retirement.

The reality is that the cost of retirement has increased significantly, to the point where some retirees may need to save above their pre-retirement income and make it last for up to 30 years. Planning for lifetime income in today’s environment generally focuses more on today’s realities instead of outdated formulas and methods.

Understanding Your True Risk Tolerance

The recent stock market volatility, the bear market, the ever-growing inflation rate, and ongoing supply issues have taken a severe toll on the American psyche. For some, it has forever altered how they perceive and manage risk.

Understanding your risk tolerance is considered one of the most important elements of investing.

Retiring Abroad

If you dream of living abroad, retirement may be the best time. Over half a million Americans living outside the US receive some Social Security, and that number is expected to grow. Many retirees cite cost of living as their reason for moving, while others say health care costs contribute to their move away from the U.S.

Managing Emotions and Expectations During Market Uncertainty

Riding the highs, and experiencing the lows, it is the way of the investment market. However, what if we told you that the key to sound and quality investing is learning how to keep it cool when the market is in turmoil? In this article, we are going to look at some of the tools that can help you manage your emotions and expectations during market uncertainty.